Navigating Market Volatility in Retirement: Lessons from Recent Turbulence

Written By: Susannah Orzolek

Market volatility is an inevitable part of life for anyone whether they are still saving for retirement or relying on investments as a crucial component of their income plan. For many retirees, the unpredictable nature of the market is one of the most daunting aspects of their financial future. The past month has served as a stark reminder of just how volatile markets can be, with prices swinging dramatically in response to geopolitical shifts and economic uncertainty.

The Current Market Landscape

Recent weeks have been a rollercoaster for investors, with markets rising and falling in rapid succession. The S&P 500 surged 2.3% on a single Thursday, marking the largest daily gain of 2024. However, just three days earlier, it experienced its biggest single-day loss of the year. This kind of fluctuation isn’t new, but it can be unsettling, especially for those in or near retirement.

Volatility has been particularly pronounced since mid-July, with the CBOE’s Volatility Index (VIX) spiking dramatically from the teens to over 65 at one point. This sharp increase reflects heightened uncertainty and the potential for further dramatic market swings.

Lessons for the Average Investor

One key takeaway from the recent market turmoil is that volatility works both ways. While it’s easy to fear the downside, it’s important to remember that volatility can also lead to significant gains. The challenge for most investors is managing the emotional response to these swings.

Tom Siomades, Chief Market Economist for AE Wealth Management, advises caution for those considering timing the market. Attempting to buy or sell at just the right moment is notoriously difficult and often leads to more harm than good. Instead, a steady, long-term approach tends to yield better results.

The Impact of Social Security Adjustments

Adding to the uncertainty, Social Security’s 2025 Cost of Living Adjustment (COLA) is expected to be lower than in recent years. Initial estimates suggest a COLA of just 2.63%, down from 3.2% in 2024 and 8.7% in 2023. For many retirees, this is concerning news. A recent survey found that 62% of retirees view the 2024 COLA as insufficient, and nearly half have considered returning to work to cover their expenses.

This situation underscores the importance of having a diversified income strategy in retirement. Relying solely on Social Security can leave retirees vulnerable, especially during periods of market volatility.

Strategies for Navigating Financial Storms

While we can’t predict or prevent market downturns, there are strategies to help mitigate their impact on your retirement. One of the most significant risks retirees face is taking withdrawals from their retirement accounts during a market downturn. This can deplete savings faster than expected and jeopardize long-term financial security.

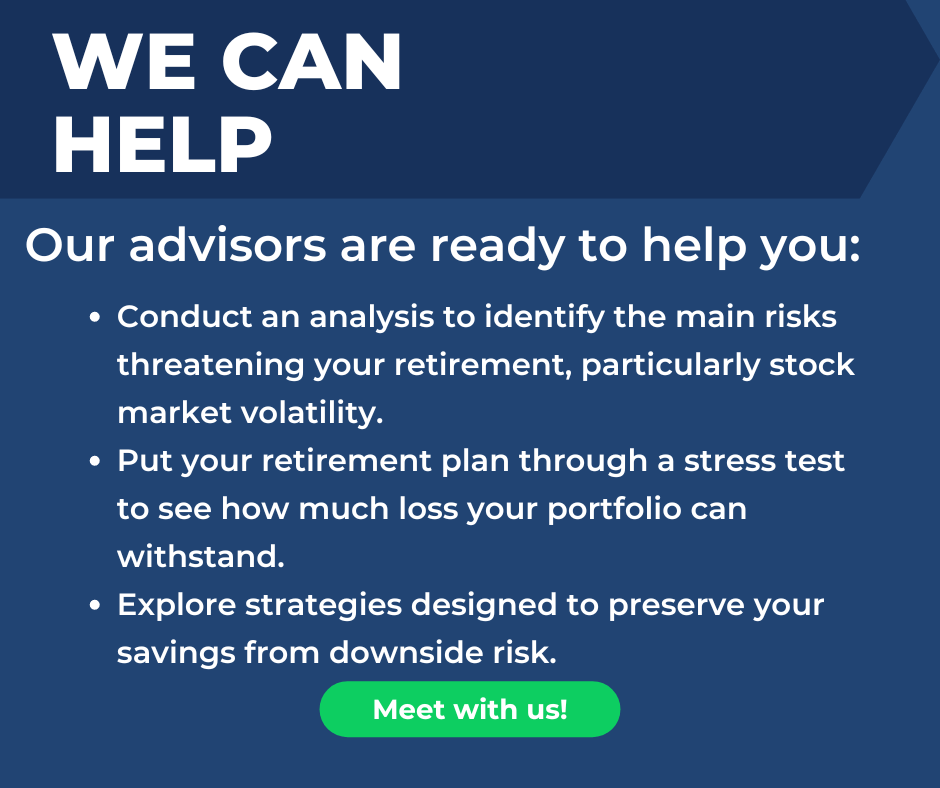

To help protect your retirement, consider the following steps:

- Risk Analysis: Conduct an analysis to identify the main risks threatening your retirement, particularly stock market volatility.

- Stress Testing: Put your retirement plan through a stress test to see how much loss your portfolio can withstand.

- Strategic Adjustments: Explore strategies designed to preserve your savings from downside risk.

By taking these proactive steps, you can gain peace of mind knowing that your retirement plan is built to withstand financial storms.

Conclusion: The Power of Preparation

In uncertain times, having the right income strategies in place is crucial. When you understand the current state of your retirement savings, you’re less likely to make panic-based decisions in response to global events. While we can’t know what the future holds for the markets, working with a financial advisor to navigate these challenges can help ensure your retirement remains on track, regardless of market conditions.

If you’re concerned about how market volatility could impact your retirement, consider reaching out for a retirement stress test. This approach emphasizes the importance of preparation and strategic planning in retirement, especially in the face of market volatility. Strategic planning will provide valuable insights into your financial future.

Say What?

A $1 million starter home is the new normal in over 200 cities

A starter home used to be considered a smaller, but more affordable option for young families and other first-time buyers looking to enter the real estate market. That may no longer be the case. These days, the typical starter home is worth at least $1 million in 237 cities, the most ever, according to new findings published by Zillow.

This week in history

1777 – The Stars and Stripes flies in battle for the first time

1963 – Martin Luther King Jr. delivers his “I Have a Dream” speech during the March on Washington

2005 – Hurricane Katrina makes landfall into the Gulf Coast

2008 – John McCain selects Sarah Palin as his running mate

2016 – Mother Teresa becomes a saint

What did it cost? (General Admission Tickets – Boston Red Sox)

1974 — $20

2004 — $44

2024 – Opening Day 2024 vs. Baltimore Orioles, Standing Room Row, $169

Have any questions? That’s what we’re here for! Call us at 844-227-5766 today!

Get on our email list to receive these updates in your inbox!

Ready to Take The Next Step?

For more information about any of the products and services listed here, schedule a free assessment today or register to attend a seminar.